Wallace Inc., a developer of radiology equipment, has stock outstanding as follows: 30,000 shares of cumulative preferred 2% stock, $90 par and 125,000 shares of $10 par common. During its first four years of operations, the following amounts were distributed as dividends:first year, $24,000; second year, $81,000; third year, $92,000; fourth year, $139,000. Calculate the dividends per share on each class of stock for each of the four years.Answer:

1st Year 2nd Year 3rd Year 4th Yeara. Total dividend declared…………… $24,000 $81,000 $92,000 $139,000Preferred dividend (current)……… $24,000 $51,000* $54,000 $ 54,000Preferred dividend in arrears……… — 30,000 3,000 —b. Total preferred dividends………… $24,000 $81,000 $57,000 $ 54,000Preferred shares outstanding…… ÷ 30,000 ÷ 30,000 ÷ 30,000 ÷ 30,000Preferred dividend per share…… $ 0.80 $ 2.70 $ 1.90 $ 1.80* $51,000 = $81,000 – $30,000Dividend for common shares(a. – b.)……………………………… $ — $ — $ 35,000 $ 85,000Common shares outstanding…… ÷ 125,000 ÷ 125,000Common dividend per share……… $ 0.28 $ 0.68

On February 25, Madison County Rocks Inc., a marble contractor, issued for cash 120,000 shares of $36 par common stock at $40, and on June 3, it issued for cash 50,000 shares of preferred stock, $8 par at $9.a. Journalize the entries for February 25 and June 3.b. What is the total amount invested (total paid-in capital) by all stockholders as of June 3?Answer:

a. Feb. 25 Cash (120,000 shares × $40) 4,800,000Common Stock (120,000 shares × $36) 4,320,000Paid-In Capital in Excess of Par—Common Stock [120,000 shares × ($40 – $36)] 480,000June 3 Cash (50,000 shares × $9) 450,000Preferred Stock (50,000 shares × $8) 400,000Paid-In Capital in Excess of Par—Preferred Stock [50,000 shares × ($9 – $8)] 50,000b. $5,250,000 ($4,800,000 + $450,000)

Lightfoot Inc., a software development firm, has stock outstanding as follows: 40,000 shares of cumulative preferred 1% stock, $125 par, and 100,000 shares of $150 par common. During its first four years of operations, the following amounts were distributed as dividends: first year, $36,000; second year, $58,000; third year, $75,000; fourth year, $124,000. Calculate the dividends per share on each class of stock for each of the four years.Answer:

1st Year 2nd Year 3rd Year 4th Yeara. Total dividend declared…………… $36,000 $58,000 $75,000 $124,000Preferred dividend (current)……… $36,000 $44,000* $50,000 $ 50,000Preferred dividend in arrears…… — 14,000 6,000 —b. Total preferred dividends…………Preferred shares outstanding……$36,000÷ 40,000$58,000÷ 40,000$56,000÷ 40,000$ 50,000÷ 40,000Preferred dividend per share……… $ 0.90 $ 1.45 $ 1.40 $ 1.25* $44,000 = $58,000 – $14,000Dividend for common shares(a. – b.)……………………………… $ — $ — $ 19,000 $ 74,000Common shares outstanding……… ÷ 100,000 ÷ 100,000Common dividend per share…… $ 0.19 $ 0.74

On August 5, Synthetic Carpet Inc., a carpet wholesaler, issued for cash 500,000 shares of no-par common stock (with a stated value of $1) at $3, and on December 17, it issued for cash 5,000 shares of preferred stock, $180 par at $200.a. Journalize the entries for August 5 and December 17, assuming that the common stock is to be credited with the stated value.b. What is the total amount invested (total paid-in capital) by all stockholders as of December 17?Answer:

a. Aug. 5 Cash (500,000 shares × $3) 1,500,000Common Stock (500,000 shares × $1) 500,000Paid-In Capital in Excess of Stated Value—Common Stock [500,000 shares × ($3 – $1)] 1,000,000Dec. 17 Cash (5,000 shares × $200) 1,000,000Preferred Stock (5,000 shares × $180) 900,000Paid-In Capital in Excess of Par—Preferred Stock [5,000 shares × ($200 – $180)] 100,000b. $2,500,000 ($1,500,000 + $1,000,000)

Heavenly Sounds Corp., an electric guitar retailer, was organized by Mickey Blessing, John Frey, and Nancy Stein. The charter authorized 750,000 shares of common stock with a par of $20. The following transactions affecting stockholders’ equity were completed during the first year of operations:a. Issued 45,000 shares of stock at par to John Frey for cash.b. Issued 400 shares of stock at par to Mickey Blessing for promotional services provided in connection with the organization of the corporation, and issued 60,000 shares of stock at par to Mickey Blessing for cash.c. Purchased land and a building from Nancy Stein in exchange for stock issued at par. The building is mortgaged for $450,000 for 20 years at 4%, and there is accrued interest of $1,500 on the mortgage note at the time of the purchase. It is agreed that the land is to be priced at $150,000 and the building at $600,000, and that Nancy Stein’s equity will be exchanged for stock at par. The corporation agreed to assume responsibility for paying the mortgage note and the accrued interest.Journalize the entries to record the transactions.Answer:

a. Cash 900,000Common Stock (45,000 shares × $20) 900,000b. Organizational Expenses 8,000Common Stock (400 shares × $20) 8,000Cash 1,200,000Common Stock (60,000 shares × $20) 1,200,000c. Land 150,000Building 600,000Interest Payable* 1,500Mortgage Note Payable 450,000Common Stock (14,925 shares × $20) 298,500* An acceptable alternative would be to credit Interest Expense.

On May 10, First Lift Corporation, a wholesaler of hydraulic lifts, acquired land in exchange for 3,600 shares of $4 par common stock with a current market price of $28. Journalize the entry to record the transaction.Answer:

May 10 Land (3,600 shares × $28) 100,800Common Stock (3,600 shares × $4) 14,400Paid-In Capital in Excess of Par—Common Stock [3,600 shares × ($28 – $4)] 86,400

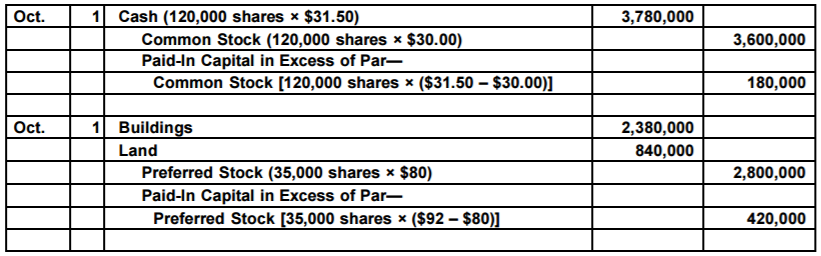

Willow Creek Nursery, with an authorization of 75,000 shares of preferred stock and 200,000 shares of common stock, completed several transactions involving its stock on October 1, the first day of operations. The trial balance at the close of the day follows:

Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,780,000Land . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 840,000Buildings. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,380,000Preferred 1% Stock, $80 par. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,800,000Paid-In Capital in Excess of Par—Preferred Stock. . . . . . . . . . . . . . . . . . . 420,000Common Stock, $30 par . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,600,000Paid-In Capital in Excess of Par—Common Stock . . . . . . . . . . . . . . . . . . . 180,0007,000,000 7,000,000All shares within each class of stock were sold at the same price. The preferred stock was issued in exchange for the land and buildings.Journalize the two entries to record the transactions summarized in the trial balance.Answer:

Oct. 1 Cash (120,000 shares × $31.50) 3,780,000Common Stock (120,000 shares × $30.00) 3,600,000Paid-In Capital in Excess of Par—Common Stock [120,000 shares × ($31.50 – $30.00)] 180,000Oct. 1 Buildings 2,380,000Land 840,000Preferred Stock (35,000 shares × $80) 2,800,000Paid-In Capital in Excess of Par—Preferred Stock [35,000 shares × ($92 – $80)] 420,000

Workplace Products Inc., a wholesaler of office products, was organized on February 1 of the current year, with an authorization of 10,000 shares of preferred 2% stock, $120 par and 250,000 shares of $25 par common stock. The following selected transactions were completed during the first year of operations:Feb. 1. Issued 180,000 shares of common stock at par for cash.1. Issued 400 shares of common stock at par to an attorney in payment of legal fees for organizing the corporation.Mar. 9. Issued 30,000 shares of common stock in exchange for land, buildings, and equipment with fair market prices of $200,000, $550,000, and $135,000, respectively.Apr. 13. Issued 8,500 shares of preferred stock at $131 for cash.Journalize the transactions.Answer:

Feb. 1 Cash 4,500,000Common Stock (180,000 shares × $25) 4,500,0001 Organizational Expenses 10,000Common Stock (400 shares × $25) 10,000Mar. 9 Land 200,000Buildings 550,000Equipment 135,000Common Stock (30,000 shares × $25.00) 750,000Paid-In Capital in Excess of Par—Common Stock [30,000 shares × ($29.50 – $25.00)] 135,000Apr. 13 Cash (8,500 shares × $131) 1,113,500Preferred Stock (8,500 shares × $120) 1,020,000Paid-In Capital in Excess of Par—Preferred Stock [8,500 shares × ($131 – $120)] 93,500

Healthy Living Co. is an HMO for businesses in the Seattle area. The following account balances appear on the balance sheet of Healthy Living Co.: Common stock (400,000 shares authorized; 300,000 shares issued), $18 par, $5,400,000; Paid-in capital in excess of par—common stock, $1,500,000; and Retained earnings, $78,000,000. The board of directors declared a 5% stock dividend when the market price of the stock was $40 a share. Healthy Living Co. reported no income or loss for the current year.a. Journalize the entries to record (1) the declaration of the dividend, capitalizing an amount equal to market value, and (2) the issuance of the stock certificates.b. Determine the following amounts before the stock dividend was declared: (1) total paid-in capital, (2) total retained earnings, and (3) total stockholders’ equity.c. Determine the following amounts after the stock dividend was declared and closing entries were recorded at the end of the year: (1) total paid-in capital, (2) total retained earnings, and (3) total stockholders’ equity.Answer:

a. (1)Stock Dividends [(300,000 shares × 5%) × $40] 600,000Stock Dividends Distributable (15,000 shares × $18) 270,000Paid-In Capital in Excess of Par—Common Stock [15,000 shares × ($40 – $18)] 330,000(2) Stock Dividends Distributable 270,000Common Stock 270,000

b. (1) $6,900,000 ($5,400,000 + $1,500,000)(2) $78,000,000(3) $84,900,000 ($6,900,000 + $78,000,000)c. (1) $7,500,000 ($5,400,000 + $1,500,000 + $270,000 + $330,000)(2) $77,400,000 ($78,000,000 – $600,000)(3) $84,900,000 ($7,500,000 + $77,400,000)

Crystal Lake Inc. bottles and distributes spring water. On March 4 of the current year, Crystal Lake reacquired 33,000 shares of its common stock at $84 per share. On August 27, Crystal Lake Inc. sold 25,000 of the reacquired shares at $90 per share. The remaining 8,000 shares were sold at $80 per share on November 11.a. Journalize the transactions of March 4, August 27, and November 11.b. What is the balance in Paid-In Capital from Sale of Treasury Stock on December 31 of the current year?c. For what reasons might Crystal Lake have purchased the treasury stock?Answer:

a. Mar. 4 Treasury Stock (33,000 shares × $84) 2,772,000Cash 2,772,000Aug. 27 Cash (25,000 shares × $90) 2,250,000Treasury Stock (25,000 shares × $84) 2,100,000Paid-In Capital from Sale of TreasuryStock [25,000 shares × ($90 – $84)] 150,000Nov. 11 Cash (8,000 shares × $80) 640,000Paid-In Capital from Sale of TreasuryStock [8,000 shares × ($84 – $80)] 32,000Treasury Stock (8,000 shares × $84) 672,000b. $118,000 ($150,000 – $32,000) creditc. Crystal Lake may have purchased the stock to support the market price of the stock, to provide shares for resale to employees, or for reissuance to employees as a bonus according to stock purchase agreements.

Irrigate Smart Inc. develops and produces spraying equipment for lawn maintenance and industrial uses. On February 17 of the current year, Irrigate Smart Inc. reacquired 50,000 shares of its common stock at $12 per share. On April 29, 31,000 of the reacquired shares were sold at $15 per share, and on July 31, 12,000 of the reacquired shares were sold at $17.a. Journalize the transactions of February 17, April 29, and July 31.b. What is the balance in Paid-In Capital from Sale of Treasury Stock on December 31 of the current year?c. What is the balance in Treasury Stock on December 31 of the current year?d. How will the balance in Treasury Stock be reported on the balance sheet?Answer:

a. Feb. 17 Treasury Stock (50,000 shares × $12) 600,000Cash 600,000Apr. 29 Cash (31,000 shares × $15) 465,000Treasury Stock (31,000 shares × $12) 372,000Paid-In Capital from Sale of TreasuryStock [31,000 shares × ($15 – $12)] 93,000July 31 Cash (12,000 shares × $17) 204,000Treasury Stock (12,000 shares × $12) 144,000Paid-In Capital from Sale of TreasuryStock [12,000 shares × ($17 – $12)] 60,000b. $153,000 ($93,000 + $60,000) creditc. $84,000 (7,000 shares × $12) debitd. The balance in the treasury stock account is reported as a deduction from the total of the paid-in capital and retained earnings.